Freight factoring is defined as the sale of unpaid freight invoices to a factoring company in exchange for immediate cash, giving trucking companies access to money they have already earned without waiting 30–90 days for brokers and shippers to pay. This process is not a loan. You are selling a receivable, which means no new debt appears on your books. For small carriers running tight margins, that distinction matters. Providers like DAT and C.H. Robinson have built factoring programs specifically around trucking workflows, making the process faster and more practical than general invoice financing.

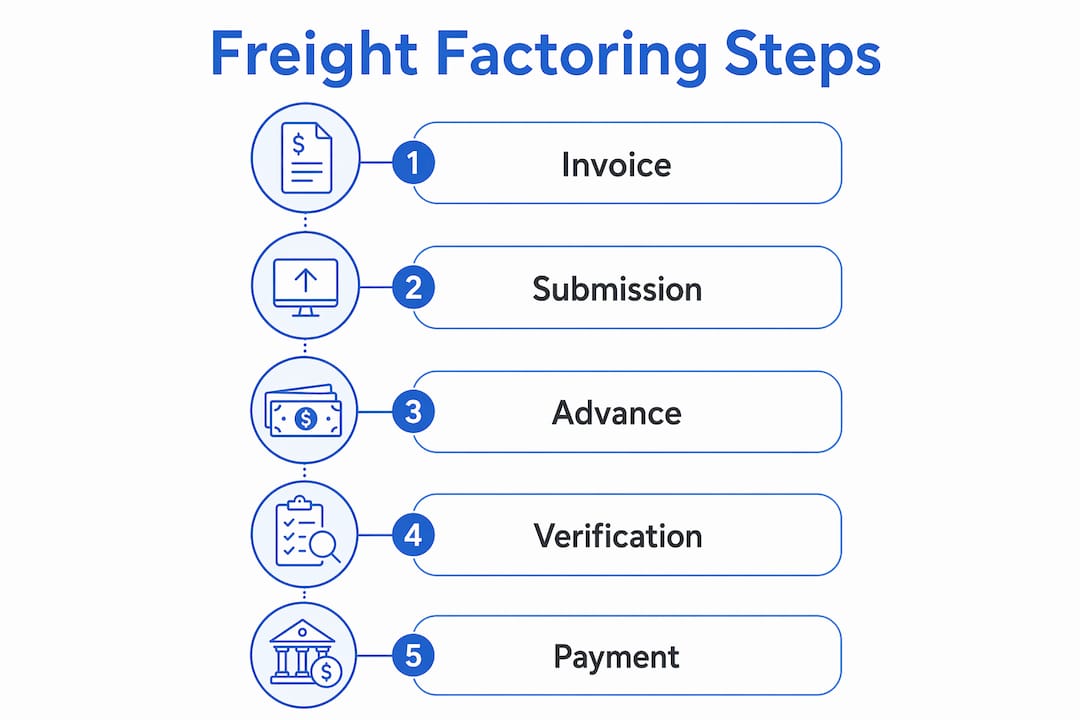

Freight factoring follows a clear, repeatable process once you understand the steps. Here is exactly what happens from delivery to deposit.

The key nuance here is recourse versus non-recourse factoring. With recourse factoring, you must repurchase the invoice if the broker fails to pay. With non-recourse factoring, the factor absorbs the loss, but only in specific situations such as broker insolvency or bankruptcy. Delivery disputes, short pays, and documentation errors are typically excluded from non-recourse coverage.

Pro Tip: Always confirm your proof of delivery is signed and dated before submitting an invoice. A missing signature is the single most common reason for verification delays.

Not all factoring programs are built the same. Understanding the main types of freight factoring solutions helps you pick the right fit for your operation.

Spot factoring vs. contract factoring

Spot factoring lets you choose which invoices to factor, one at a time, with no long-term commitment. Contract factoring requires you to factor most or all of your invoices, typically under agreements running 12–24 months. Spot factoring offers flexibility. Contract factoring usually comes with lower fees and more bundled tools because you are committing volume.

Recourse vs. non-recourse factoring

| Type | Who Bears Credit Risk | Coverage Scope | Typical Fee |

|---|---|---|---|

| Recourse | Carrier repurchases unpaid invoices | All non-payment events | Lower |

| Non-recourse | Factor absorbs loss | Insolvency or bankruptcy only | Higher |

Non-recourse sounds safer, but the protection is narrower than most carriers expect. Read the contract carefully before assuming you are fully covered.

Trucking-specific vs. general invoice factoring

Freight factoring providers understand lane cycles, broker credit ratings, and load documentation in ways that general invoice factors do not. Trucking-specific factors offer add-ons that general providers skip entirely:

These tools reduce your administrative workload and protect you from hauling for brokers who are slow to pay or financially unstable.

Pro Tip: Before signing with any factor, run a broker credit check through the provider’s platform. A broker with a poor payment history can cost you more than the factoring fee saves you.

Freight factoring costs center on three numbers: the advance rate, the discount rate, and the reserve.

The advance rate is the percentage of the invoice the factor pays you upfront. Advance rates commonly run 70–95%, with most carriers landing in the 80–90% range. A higher advance rate means more cash in your pocket immediately, but it does not tell the full story.

The discount rate is the factoring fee, expressed as a percentage of the invoice value. Fees typically fall between 1–5% per invoice, with most carriers paying 1.5–4%. On a $2,000 invoice with a 3% fee, you pay $60 to access your money faster. That cost adds up across hundreds of loads per year, so comparing rates across providers is worth your time. You can review a detailed breakdown of how these numbers interact at factoring rates for truckers.

The reserve is the portion held back until the broker pays. Once payment clears, the factor releases the reserve minus the fee. Here is a simple example:

| Invoice Value | Advance Rate | Advance Paid | Fee (3%) | Reserve Released |

|---|---|---|---|---|

| $2,000 | 90% | $1,800 | $60 | $140 |

| $5,000 | 85% | $4,250 | $150 | $600 |

Watch for these additional cost drivers in your contract:

Freight factoring is not the only way to access working capital, but it solves a specific problem that bank loans and quick pay programs do not address as directly.

Freight factoring vs. bank loans

A bank loan adds debt to your balance sheet and requires a credit check, collateral, and weeks of processing time. Factoring adds no debt. You are converting an asset you already own, a paid invoice, into cash. Approval depends on your broker’s creditworthiness, not yours. That makes factoring accessible to newer carriers who cannot qualify for traditional financing.

Freight factoring vs. quick pay programs

Many brokers offer quick pay options that release funds within a few days for a fee, typically 1–3% of the load. Quick pay is simple, but it only works load by load through that specific broker. Factoring gives you a consistent cash flow system across all your brokers, plus back-office support and broker credit tools that quick pay programs do not include.

Freight factoring vs. accounts receivable financing

Accounts receivable financing uses your invoices as collateral for a loan. You still own the invoices and still owe repayment. With factoring, you sell the invoices outright. The cost structure differs too. Financing carries interest. Factoring carries discount rates and reserves. Neither is universally cheaper. The right choice depends on your volume, broker mix, and how much back-office support you need.

Pro Tip: If you haul for a small number of high-volume brokers, quick pay may be cheaper. If you work with 10 or more brokers regularly, factoring typically saves time and reduces collection risk.

Factoring works best when you treat it as a system, not just a cash advance tool. These practices protect your margins and keep the process running without friction.

Reducing trucking operational costs goes beyond factoring fees. Fuel, maintenance, and insurance all affect how much cash you actually keep after factoring. Build your financial picture around all of these variables together.

Freight factoring converts unpaid invoices into same-day cash, giving small carriers the liquidity to cover fuel, payroll, and maintenance without taking on debt.

| Point | Details |

|---|---|

| Factoring is not a loan | You sell receivables, so no debt appears on your balance sheet. |

| Advance rates vary | Expect 70–95% of invoice value upfront; fees typically run 1.5–4%. |

| Non-recourse has limits | Coverage usually applies only to broker insolvency, not disputes or short pays. |

| Trucking-specific factors add value | Fuel cards, broker credit checks, and back-office tools are included with freight-focused providers. |

| Contract terms determine real cost | Minimum volumes, chargebacks, and termination fees affect total cost beyond the advertised rate. |

Most small trucking owners come to factoring because they are out of options. A broker owes them $8,000, fuel is due, and the bank said no. Factoring solves that immediate crisis. But the carriers who get the most out of it are the ones who treat it as a permanent cash flow tool, not an emergency measure.

The biggest mistake I see is signing a contract factoring agreement without reading the recourse clause. Carriers assume non-recourse means they are fully protected. They are not. Non-recourse coverage is narrowly defined. If a broker disputes a delivery or short pays an invoice, that risk stays with you in most contracts.

The second mistake is ignoring broker concentration limits. If 70% of your volume runs through one broker and your contract caps concentration at 50%, you will hit a wall fast. Diversify before you factor, not after.

The carriers I have seen grow steadily with factoring share one habit. They use the broker credit check tool every single time before accepting a load. That one step eliminates most collection problems before they start.

Factoring is worth it for most small carriers running more than 10 loads per month. Below that volume, quick pay programs may cost less. Above it, the back-office support and consistent cash flow justify the fee. Use it as part of a broader financial plan, not as a substitute for one.

— Managment

Goeldhub built its factoring program specifically for small trucking operations that need fast cash without complicated contracts or surprise fees.

With Goeldhub’s freight factoring services, you get same-day invoice advances, transparent discount rates, and a team that understands trucking paperwork from rate confirmations to proof of delivery. The platform pairs factoring with fuel card discounts, ELD compliance tools, and freight rate analytics, so you manage cash flow and operational costs from one place. For $15 per driver per month, you access the full platform including factoring support. Start with a 14-day free trial and see how much faster your cash moves.

Freight factoring is when a trucking company sells its unpaid invoices to a factoring company for immediate cash instead of waiting 30–90 days for brokers to pay. It is not a loan. You are converting money you have already earned into cash you can use today.

Factoring companies typically advance 80–95% of the invoice value upfront, with fees running 1.5–4% per invoice. The remaining balance is released after the broker pays.

Freight factoring is worth it for carriers running consistent volume who cannot afford to wait on slow broker payments. The fees are real, but the back-office support, broker credit tools, and same-day funding often outweigh the cost for operations running 10 or more loads per month.

With recourse factoring, you must repurchase the invoice if the broker does not pay. With non-recourse factoring, the factor absorbs the loss, but only in cases of broker insolvency or bankruptcy. Most disputes and short pays are excluded from non-recourse coverage.

Most freight factoring companies fund within 24 hours after you submit your invoice and proof of delivery. Many providers offer same-day funding once your account is set up and your documentation is clean.