A factoring rate is the fee a trucking company pays to convert unpaid invoices into immediate cash, expressed as either a fixed percentage of the invoice value or a decimal multiplier applied to the funded amount. For owner-operators and small fleets, this rate directly determines how much a load actually earns after financing costs. Typical factoring rates for trucking businesses range from 1% to 5% per month, with freight industry averages clustering around 2.5%. Understanding this number, and everything attached to it, is the difference between factoring working for your business and quietly draining your margins.

A factoring rate is defined as the discount fee a factoring company charges in exchange for purchasing your unpaid invoice at a reduced value. The industry also uses the term “factor rate” when referring to merchant cash advances, where the fee appears as a decimal multiplier ranging from 1.10 to 1.50. Both forms represent a fixed cost, not a variable interest rate that compounds over time.

This distinction matters more than most owner-operators realize. With a traditional bank loan, paying early reduces your total interest cost. With factoring, the fee is locked in at the time of the transaction. Early repayment does not reduce the total factoring cost. You pay the agreed fee regardless of whether your customer settles in 15 days or 45 days, which is why understanding the full structure before signing is so critical.

In invoice factoring, the factoring company buys your freight invoice, advances you a percentage of its value immediately, and collects from your broker or shipper directly. The factoring rate is the fee deducted from the remaining balance when the invoice is paid. For a trucking business running on tight margins, even a half-percent difference in rate can add up to thousands of dollars annually across a fleet.

The calculation method depends on whether you are using invoice factoring or a merchant cash advance. For invoice factoring, the formula is straightforward.

For merchant cash advances, the factor rate multiplier works differently. A $50,000 advance at a 1.4 factor rate means you repay $70,000 total, regardless of how quickly you pay it back. That fixed cost structure is what separates factor rate financing from APR-based loans.

One number that changes the math significantly is whether the factoring fee applies to the full invoice face value or only to the advance amount. Two providers charging similar rates can produce very different total costs depending on this fee base. Always ask which amount the percentage applies to before comparing quotes.

Pro Tip: Run the same sample invoice through every provider you evaluate, using your typical broker payment window of 30 or 45 days. This gives you a real cost comparison rather than a headline rate comparison.

Understanding the base factoring rate is only the starting point. The actual cost of factoring includes several components that vary by provider and contract structure.

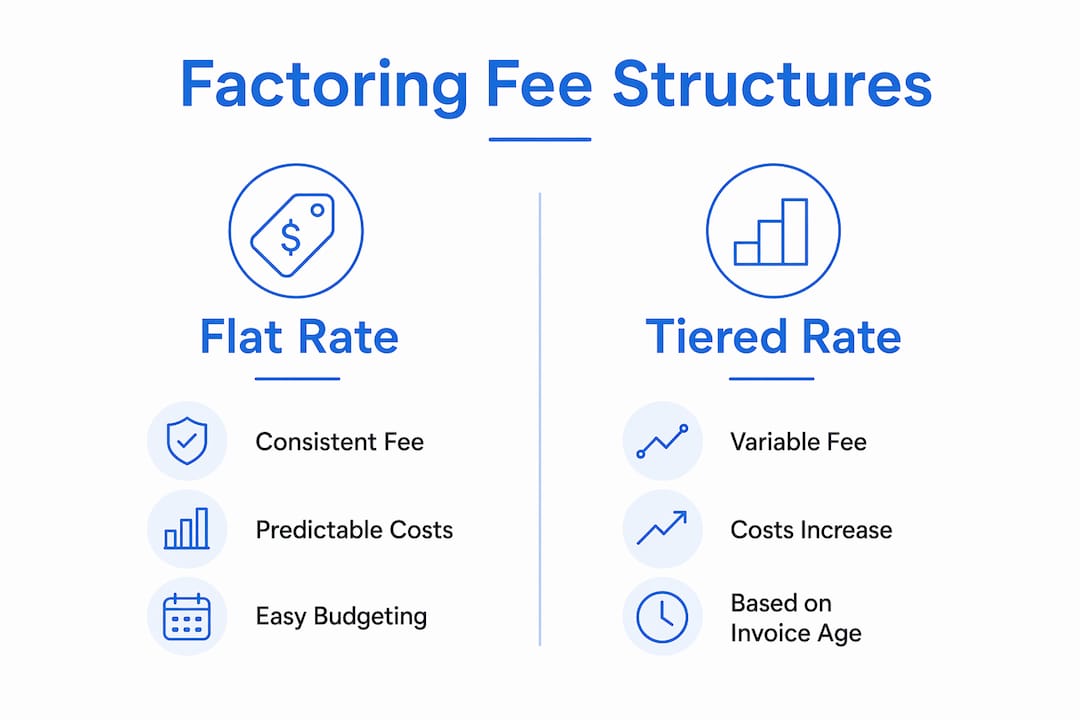

Flat rate model: You pay the same percentage regardless of how long the invoice remains unpaid. Predictable and easy to budget, but potentially expensive if your brokers pay quickly.

Tiered or time-based model: The fee increases as the invoice ages. A common structure charges 1.5% for the first 30 days plus 0.5% for each additional 10-day period. If your broker pays on day 50, your effective rate climbs to 2.5%. This model rewards fast-paying customers and penalizes slow ones.

Beyond the base rate, all-in factoring costs include setup fees, processing fees, wire or ACH transfer charges, monthly minimums, and sometimes early termination penalties. These add-ons can push your effective cost several percentage points above the advertised rate. A provider quoting 2% with a $25 wire fee on a $1,000 invoice is actually charging 4.5% all-in.

Here is a comparison of the two primary fee structures:

| Feature | Flat rate | Tiered rate |

|---|---|---|

| Cost predictability | High | Low to moderate |

| Best for slow-paying brokers | Yes | No |

| Best for fast-paying brokers | No | Yes |

| Risk of cost creep | Low | High |

| Ease of budgeting | Simple | Requires tracking |

Pro Tip: Ask every factoring company for a complete fee schedule in writing before signing. If they hesitate or say fees are “case by case,” that is a red flag.

You can also find freight industry cost breakdowns that help you benchmark what a fair all-in rate looks like for your lane and volume.

Owner-operators often treat the factoring rate and the advance rate as the same thing. They are not, and confusing the two leads to poor cash flow decisions.

The advance rate is the percentage of the invoice value the factoring company pays you upfront, before the broker or shipper settles the invoice. Advance rates typically range from 70% to 95% depending on the arrangement, your customer’s credit profile, and the factoring company’s policies. The factoring rate is the separate fee charged for the service.

Here is why both numbers matter together:

Consider a $4,000 invoice. Provider A offers 90% advance at 3% fee: you get $3,600 upfront and pay $120 in fees. Provider B offers 80% advance at 2.5% fee: you get $3,200 upfront and pay $100 in fees. Provider A gives you $400 more immediately but costs $20 more. If you need that cash today to cover fuel or a repair, Provider A may be worth the premium. If cash flow is stable, Provider B saves money over time.

Pro Tip: Calculate your “effective advance” by subtracting the factoring fee from the advance amount. This gives you the true cash you walk away with per invoice, which is the number that actually matters for operations.

Getting the best factoring rate requires more than calling three companies and picking the lowest number. Here is a practical process for owner-operators and small fleets.

Factoring fees vary with perceived industry risk and volume. Trucking companies with strong payment histories and consistent invoice volume can negotiate better terms. If you have been in business for two or more years with clean receivables, use that as leverage.

For a broader view of cash flow strategies that complement factoring, including fuel card programs and expense management, Goeldhub’s resource library covers the full picture for small fleets.

A factoring rate is a fixed fee, not an interest rate, and understanding its full structure, including advance rates, fee bases, and add-on charges, determines whether factoring actually improves your cash flow or quietly erodes it.

| Point | Details |

|---|---|

| Factoring rate definition | A fixed percentage or multiplier fee charged on invoice value or funded amount. |

| Flat vs. tiered structures | Tiered rates increase as invoices age, making slow-paying brokers more expensive to factor. |

| Advance rate is separate | The advance rate determines upfront cash; the factoring rate determines total cost. |

| All-in cost matters | Add-on fees like wire charges and monthly minimums can double the effective rate. |

| Negotiation is possible | Strong payment history and invoice volume give you leverage to cut factoring costs. |

Most owner-operators I talk to focus entirely on the headline factoring rate. They hear “2.5%” and sign the contract. What they miss is the fee base, the wire charges, and the tiered structure that kicks in when a broker pays on day 35 instead of day 28. By the time the reserve is released, the effective rate is closer to 4.5%, and they have no idea why their cash flow still feels tight.

The uncomfortable truth is that factoring companies are not required to present their costs the way banks present APR. There is no standardized disclosure format. That puts the burden entirely on you to ask the right questions and model the real numbers before committing.

I have also seen truckers avoid factoring entirely because they assume all providers are the same. That is equally costly. When a broker takes 45 days to pay and you need fuel money today, factoring at 3% all-in is far cheaper than a high-interest short-term loan or missing a load because your truck is sitting at a fuel stop. The tool is not the problem. Using it without understanding the cost structure is.

The truckers who manage this well treat factoring like any other operating cost. They know their per-invoice factoring expense the same way they know their cost per mile. That clarity lets them price loads correctly, choose the right brokers, and decide when factoring makes sense versus when they can wait for direct payment.

— Management

Goeldhub’s factoring services are designed specifically for small trucking companies and owner-operators who need fast cash without complicated fee structures. You get transparent rates, no hidden charges, and a team that understands freight operations. Goeldhub connects you to factoring solutions that fit your invoice volume and cash flow needs, with the same platform that handles your ELD compliance, fuel card discounts, and driver management. For $15 per driver per month, you get access to all of it. Start with a 14-day free trial and see exactly what your factoring costs should look like.

A factoring rate is the fee a factoring company charges to advance cash against your unpaid freight invoices, expressed as a percentage of the invoice value. Rates typically range from 1% to 5% per month depending on volume, customer creditworthiness, and contract terms.

A factoring fee is a fixed cost applied to the invoice or funding amount at the time of the transaction. Unlike a loan, early repayment does not lower the total fee you owe.

The advance rate is the percentage of the invoice paid to you upfront, typically 70% to 95%. The factoring rate is the separate fee charged for the service. Both numbers affect your cash flow and total cost.

All-in factoring costs include setup fees, wire or ACH transfer charges, monthly minimums, and early termination penalties. These add-ons can significantly increase your effective rate above the advertised percentage.

Yes. Factoring companies adjust rates based on invoice volume, industry risk, and payment history. Trucking companies with consistent loads and reliable broker relationships have real leverage to negotiate lower fees.