Invoice factoring in trucking is defined as selling your unpaid freight invoices to a third party, called a factoring company, in exchange for immediate cash. Instead of waiting 30–90 days for a broker to pay, you get most of that money within 24 hours. For owner-operators and small fleets running tight margins, that cash flow gap hurts. Invoice factoring trucking explained clearly is the difference between keeping your wheels turning and sitting idle waiting on a check.

The process follows a clear sequence. Once you understand each step, the whole system makes sense.

Factoring is not a loan. You are selling an asset, which is your invoice, not borrowing against it. That distinction matters because factoring does not add debt to your balance sheet. Your approval depends on the broker’s creditworthiness, not your personal or business credit score. That makes it accessible for new carriers who have not yet built a credit history.

Pro Tip: Always confirm the broker is approved by your factoring company before you accept a load. If the broker has poor credit, the factor may reject the invoice and leave you waiting for payment anyway.

Trucking invoice financing solves one specific problem: the gap between when you deliver a load and when you actually get paid. The benefits go beyond just speed.

Factoring fees typically run 1–5% per invoice, depending on broker quality, volume, and your contract terms. That sounds manageable on a single invoice. The problem is compounding. When you factor every invoice across dozens of loads per month, the effective annual cost can reach 18–60%. That is far higher than a traditional bank loan.

Many carriers underestimate how quickly factoring fees add up. A 3% fee on a $2,000 invoice is $60. Factor 20 invoices a month and you are paying $1,200 monthly just in fees. That cost deserves a line in your budget.

Watch for exclusivity clauses too. Many factoring contracts require you to factor all your invoices or a set portion of them exclusively through that company. That limits your flexibility to switch providers or use other financing tools as your business grows. Read every contract term before you sign.

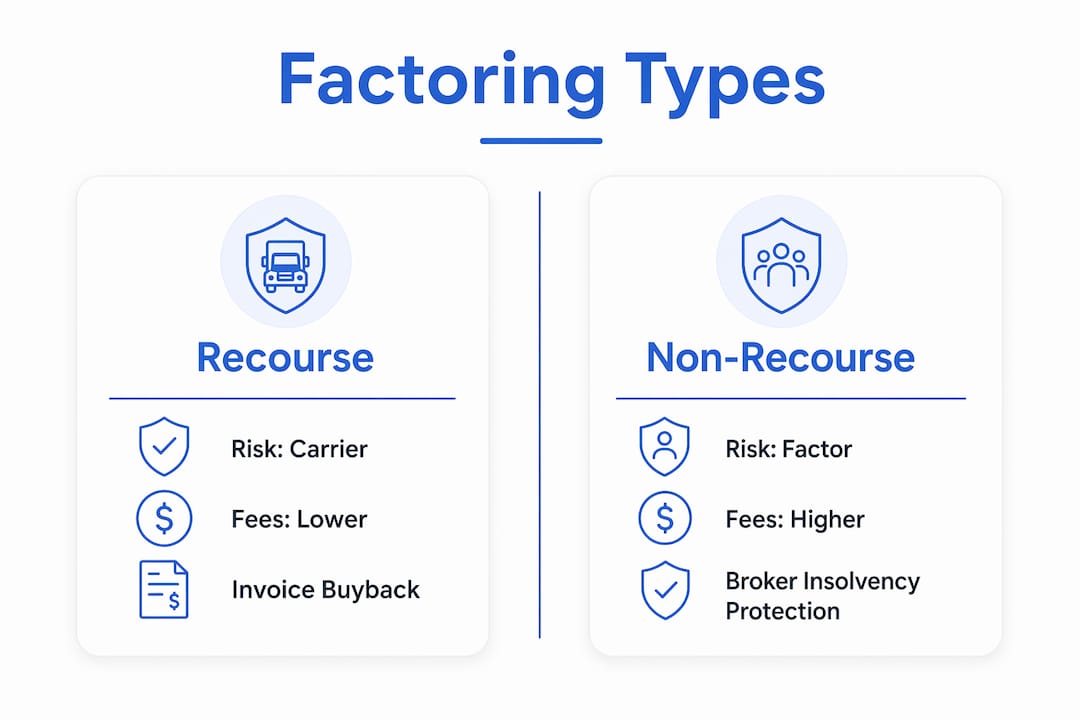

The type of factoring contract you choose determines who takes the loss if a broker does not pay.

| Feature | Recourse factoring | Non-recourse factoring |

|---|---|---|

| Who bears the risk | You, the carrier | The factoring company |

| Fee level | Lower | Higher by 0.5–1.5% |

| Coverage | All non-payment situations | Broker insolvency only |

| Best for | Carriers with reliable brokers | Carriers wanting credit protection |

With recourse factoring, if the broker fails to pay, you must buy back the invoice or repay the advance. The fees are lower because the factor carries less risk. With non-recourse factoring, the factor absorbs the loss if the broker goes bankrupt. However, non-recourse coverage typically excludes disputes or claims, meaning if a broker refuses to pay because of a delivery dispute, you may still be on the hook.

Non-recourse factoring costs more, but it provides real protection from broker insolvency. For small operators hauling for unfamiliar brokers, that protection is worth the extra fee.

Pro Tip: Before choosing non-recourse factoring, read the exact definition of “insolvency” in the contract. Some factors define it narrowly, which limits your actual protection.

This is where the invoice factoring vs bank loan trucking question gets practical. Both solve a cash flow problem, but they work very differently.

| Criteria | Invoice factoring | Bank line of credit |

|---|---|---|

| Approval basis | Broker credit | Your business credit score |

| Speed of funding | Same day to 24 hours | Days to weeks |

| Cost (effective annual) | 18–60% | 9–16% |

| Debt added | No | Yes |

| Best for | New carriers, fast cash needs | Established carriers with good credit |

| Flexibility | Limited by exclusivity clauses | Draw and repay as needed |

Bank lines of credit carry an effective annual rate of 9–16% APR, which is significantly lower than factoring over the long term. The catch is that banks require established business credit, tax returns, and financial history. A carrier in their first year rarely qualifies.

Factoring fills that gap. You do not need a credit history. You need invoices from creditworthy brokers. That makes it the right starting tool for new owner-operators. The smart move is to use factoring while you build your business credit, then transition to bank financing once you qualify. Paying 18–60% annually when a 10% line of credit is available is money left on the table.

Factoring is also invoice-based, meaning you can only factor amounts already invoiced. You cannot factor future loads or anticipated revenue. Plan your cash needs around actual delivered freight, not projected loads.

Getting the most from trucking cash flow solutions comes down to discipline in paperwork, contract awareness, and long-term planning.

Pro Tip: Ask your factoring company for a monthly fee summary. Seeing the total cost in one number makes it easier to decide when you are ready to switch to cheaper financing.

Invoice factoring gives trucking companies immediate cash by selling freight invoices, but the long-term cost requires a clear exit strategy toward lower-cost financing.

| Point | Details |

|---|---|

| Advance rate and speed | Factors advance 70–97% of invoice value, often within 24 hours of submission. |

| No debt on your books | Factoring is an asset sale, so it does not add liabilities or require a credit score check on you. |

| Real cost is higher than it looks | Effective annual costs can reach 18–60%, far above bank loan rates of 9–16%. |

| Recourse vs non-recourse matters | Non-recourse costs 0.5–1.5% more but protects you if a broker goes bankrupt. |

| Plan your exit | Use factoring to build credit, then transition to a bank line of credit to save money long-term. |

Most carriers I have worked with start factoring out of necessity, not strategy. The cash flow gap is real, and factoring solves it fast. The problem comes six months later when they realize they have been paying 30–40% annually in fees without noticing.

The carriers who use factoring well treat it like a bridge, not a permanent solution. They use the immediate cash to stay current on fuel and maintenance, build a small reserve, and work on their business credit in parallel. Within 12–18 months, many qualify for a bank line of credit and cut their financing costs by more than half.

The other thing most articles skip is the value of non-recourse factoring for small operators. Yes, it costs more per invoice. But one broker insolvency can wipe out weeks of profit for a single-truck operation. The extra 1% per invoice is cheap insurance when you are hauling for brokers you do not know well.

My honest advice: read every line of your factoring contract before you sign. Exclusivity clauses are the most common trap. Some contracts lock you in for 12 months and require you to factor every invoice. That removes your flexibility exactly when you need it most. Negotiate those terms upfront or walk away.

— Managment

Small carriers should not have to choose between fast cash and high fees. Goeldhub’s invoice factoring service is built specifically for owner-operators and small fleets, with low fees, fast funding, and no hidden exclusivity traps.

Goeldhub combines factoring with FMCSA-compliant ELD services, fuel card programs with negotiated discounts, freight rate analytics, and driver recruiting support. All of it is available for $15 per driver per month, with a 14-day free trial and no obligation. You get the cash flow tools and the compliance tools in one place, with US-based multilingual support when you need it. Visit Goeldhub’s services page to see the full platform.

Invoice factoring in trucking is the sale of unpaid freight invoices to a factoring company for immediate cash. The factor advances 70–97% of the invoice value, often within 24 hours, and collects payment directly from the broker.

Factoring fees typically run 1–5% per invoice. The effective annual cost can reach 18–60% depending on invoice frequency and fee structure, which is higher than most bank financing options.

Recourse factoring holds the carrier responsible if the broker does not pay, with lower fees. Non-recourse factoring transfers that risk to the factor but costs 0.5–1.5% more and usually covers broker insolvency only.

Yes. Factoring approval is based on the broker’s credit, not the carrier’s. New owner-operators with no business credit history can qualify as long as they haul for creditworthy brokers.

Carriers should transition to a bank line of credit once they have established business credit and at least one to two years of financial history. Bank lines carry 9–16% APR, which is far cheaper than the effective annual cost of factoring.