Factoring receivables for owner operators is defined as selling outstanding freight invoices to a third-party finance company in exchange for an immediate cash advance, typically 80–98% of the invoice value within 24 hours. The industry term is “invoice factoring” or “freight factoring,” and it exists specifically to solve the 30–90 day payment gap that brokers impose on carriers. Unlike a loan, factoring carries no APR, no monthly payments, and no debt on your balance sheet. The cost is a factoring fee of 1%–5%, deducted from the invoice settlement. For owner-operators running tight on fuel money between loads, that distinction matters enormously.

Freight factoring converts your unpaid invoices into working capital the same day you deliver a load. You submit the invoice and supporting documents to a factoring company, and they advance you the bulk of the invoice value immediately. The factor then collects payment directly from the broker or shipper. When the broker pays in full, the factor releases the remaining reserve balance to you, minus the factoring fee.

The cash flow benefit is direct and measurable. Brokers routinely pay on net-30 to net-90 terms. That gap can leave you short on fuel, insurance premiums, and truck payments before your next load even pays out. Factoring fees of 2%–3% are often cheaper than missing a load because your account is dry, or paying high-interest rates on a credit line.

Factoring also differs structurally from broker QuickPay programs. QuickPay can take up to 5 days and typically charges a fee on top of that delay. A well-run factoring arrangement funds you in 4 hours or less with same-day submissions.

Qualifying for freight factoring is more accessible than most owner operators expect. The primary underwriting factor is the creditworthiness of your broker, not your personal FICO score. Sub-600 FICO scores can still qualify, provided the brokers you haul for have solid payment histories. Factors run fraud checks and bankruptcy screenings on brokers, not on you.

You do need to own your receivables outright. That means you are operating as a 1099 independent contractor or as an LLC with authority, and no other party has a lien on your invoices. Here is what you typically need to submit:

Fleet size rarely disqualifies a single-truck owner operator. Most factoring programs accept one-truck operations from day one. Operational history matters more for volume-based pricing tiers than for basic approval.

One important distinction affects your risk exposure. Recourse factoring means you are responsible if the broker does not pay. Non-recourse factoring shifts that risk to the factor. Non-recourse protection costs roughly 0.5%–1% more per invoice but acts as insurance against broker bankruptcy on large loads. You can read a full breakdown of recourse vs. non-recourse factoring to decide which structure fits your risk tolerance.

Pro Tip: Before applying, pull a payment history report on your top three brokers. Factors approve faster when you haul for brokers with clean payment records.

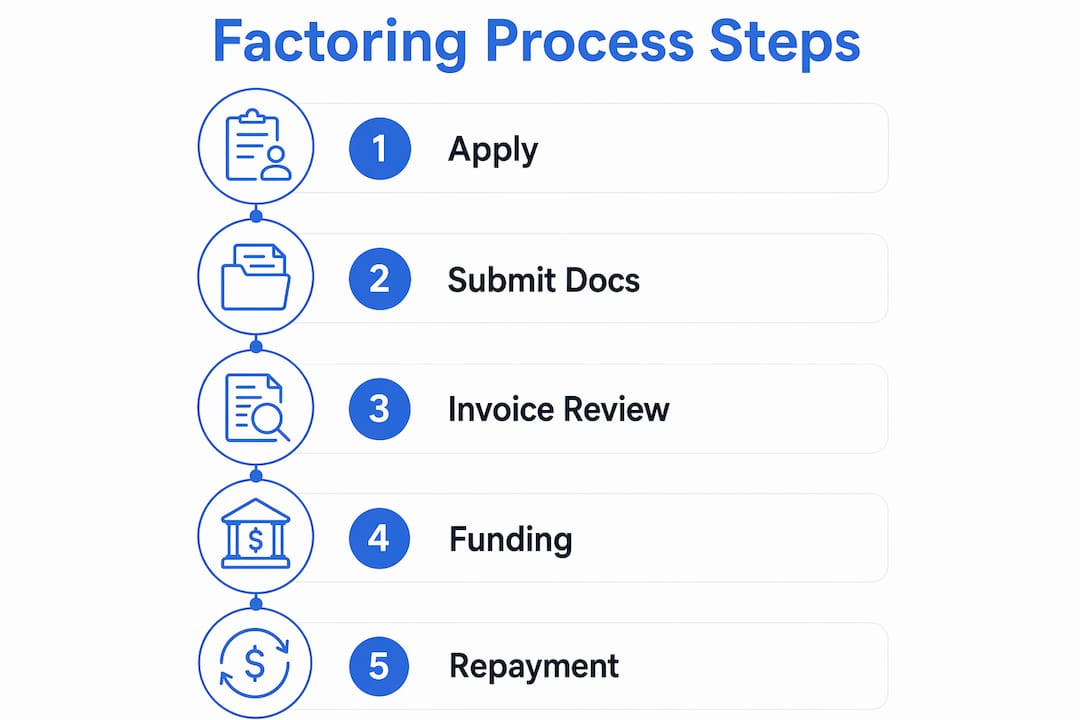

Starting freight factoring takes less time than most owner operators expect. The process from application to first funding typically runs 24–72 hours.

Choose a factoring program. Look for transparent fee structures, no long-term lock-in contracts, same-day funding capability, and value-added services like fuel cards or back-office support. Avoid programs with hidden fees on wire transfers or monthly minimums that penalize low-volume months.

Complete your application. Submit your carrier authority, W-9, voided check for ACH deposits, and a list of the brokers you regularly haul for. The factor will verify broker creditworthiness during this step.

Submit your first invoice. After approval, upload your rate confirmation, BOL, and POD through the factor’s portal or app. Documentation like a clean BOL and signed POD is required before any advance is released.

Hit the funding cutoff. Same-day funding cutoffs typically fall between 11:00 AM and 12:00 PM Eastern. Submit before that window and your advance hits the same business day. Submit after it and you receive funds the next banking morning.

Receive your advance. The factor deposits 80%–98% of the invoice value directly into your bank account or fuel card.

Reserve release. Once the broker pays the factor in full, the remaining balance (minus the factoring fee) is released to you.

| Step | Action | Typical Timeline |

|---|---|---|

| Application | Submit carrier docs and broker list | 24–72 hours |

| Invoice submission | Upload BOL, POD, rate confirmation | Same day |

| Advance funding | Receive 80%–98% of invoice value | Within 4–24 hours |

| Reserve release | Remaining balance paid after broker pays | 30–90 days |

The core benefit of freight factoring is simple. Factoring converts slow-paying invoices into immediate working capital, letting you cover fuel, insurance, and daily operating costs without waiting on broker payment cycles. That keeps your truck moving instead of sitting idle while you wait for a check.

Beyond cash flow, factoring removes the collections burden entirely. You no longer chase brokers for payment, dispute late invoices, or manage accounts receivable manually. The factor handles all of that. Many factoring programs also include fuel cards, back-office support, and load management tools that extend the value well past a simple cash advance.

The honest cost picture looks like this:

Factoring fees of 2%–3% are often cheaper than the cost of missing a load due to a cash shortfall, or paying high-interest rates on a short-term credit line.

The main risk with recourse factoring is broker default. If a broker goes bankrupt or disputes the invoice, you owe the advance back. Non-recourse factoring eliminates that exposure on qualifying invoices. Understanding factoring rates and fees before you sign any contract protects you from surprises.

Factoring works best as a growth tool, not a lifeline for covering persistent losses. Financial experts advise using factoring during predictable revenue growth phases, such as when you are adding a second truck, taking on higher-volume lanes, or scaling into contract freight. Using it to paper over poor load selection or chronic underbidding creates a fee drain with no upside.

Good broker relationships directly improve your factoring results. Brokers with clean payment histories get approved faster, and some factors offer lower rates for invoices from preferred brokers. Keeping your documentation tight, signed PODs submitted the same day as delivery, and rate confirmations filed before dispatch, cuts approval time and reduces the chance of funding delays.

Here are the practices that separate owner operators who grow with factoring from those who stagnate:

Pro Tip: Set a target: reduce the percentage of invoices you factor by 10% each quarter as your cash reserves grow. Factoring should shrink as your business matures, not expand.

Freight factoring is the most practical owner operator financing tool for closing the broker payment gap, but its long-term value depends entirely on how deliberately you use it.

| Point | Details |

|---|---|

| Immediate cash access | Factoring advances 80%–98% of invoice value within 24 hours, replacing 30–90 day waits. |

| Credit is not the barrier | Broker creditworthiness drives approval, so sub-600 FICO scores can still qualify. |

| Non-recourse protects you | Paying 0.5%–1% more for non-recourse coverage eliminates broker default risk on large invoices. |

| Timing controls funding speed | Submit invoices before the 11:00 AM–12:00 PM Eastern cutoff to receive same-day funding. |

| Use factoring to scale, not survive | Factoring works best during growth phases, not as a fix for persistent cash shortfalls. |

I have watched owner operators treat factoring as a permanent crutch and others use it to double their revenue in 18 months. The difference is almost never the factoring program itself. It is the mindset going in.

The operators who win with factoring treat the fee as a cost of doing business during a specific growth window, not as a permanent tax on every invoice. They factor aggressively when they are scaling, then pull back as their cash position strengthens. That discipline is rare, but it is the only approach that actually builds a business.

The industry has also changed. Factoring programs in 2026 are faster, more integrated, and more transparent than they were five years ago. Same-day funding is now standard, not a premium feature. Fuel cards, FMCSA compliance tools, and back-office support are bundled into many programs at no extra cost. If your current factoring arrangement does not include those services, you are leaving money on the table.

One thing I tell every owner operator: read the termination clause before you sign anything. Some contracts lock you in for 12 months with steep exit fees. Others are month-to-month. That single clause can cost you thousands if your business needs change and you are stuck in a contract that no longer fits.

Factoring is a real financial tool with real costs. Use it with a plan, and it pays for itself. Use it without one, and the fees quietly eat your margin.

— Managment

Owner operators who want fast invoice funding without the complexity of managing multiple vendors can find both in one place.

Goeldhub offers low-fee factoring solutions built for small and mid-sized trucking operations, with transparent pricing and no hidden transfer fees. The platform pairs factoring with FMCSA-compliant ELD services, fuel card programs with negotiated discounts, and driver log management, all for $15 per driver per month. Goeldhub supports existing hardware including PT-30 and IOSix devices, so you do not need to replace equipment to switch. A 14-day free trial with no obligation is available, backed by multilingual US-based customer support. Visit the Goeldhub services page to see the full list of tools available to your operation.

Freight factoring is a financial service where an owner operator sells unpaid freight invoices to a factoring company in exchange for an immediate cash advance of 80%–98% of the invoice value. The factor collects payment from the broker and releases the remaining balance, minus a fee of 1%–5%.

Your personal credit score is not the primary factor in approval. Factoring companies evaluate the creditworthiness of the brokers you haul for, which means owner operators with sub-600 FICO scores can still qualify.

You need a signed rate confirmation, a clean bill of lading, proof of delivery, your carrier authority, and a W-9. Missing or disputed documentation is the most common reason for funding delays.

Recourse factoring requires you to repay the advance if the broker does not pay. Non-recourse factoring shifts that risk to the factor at an additional cost of roughly 0.5%–1% per invoice, protecting you against broker bankruptcy.

Advanced factoring platforms can fund within 4 hours for same-day submissions made before the 11:00 AM–12:00 PM Eastern cutoff. Submissions after that window receive funding the next banking morning.